Official press announcement

Market Report July 2021

Rarely have we seen such a constellation on the stainless steel market. Prices have exploded in the first half of the year and this time it is not (only) due to the nickel price (as in 2007). The nickel price has risen by 10% since the beginning of the year, while the chrome price has increased by almost 40% and the molybdenum price by 80%. The mills' base prices, which have almost doubled in many alloys, especially in the second quarter, have the strongest impact on the transaction prices. Shortages prevail even though production volumes have increased by 30% compared to the second quarter of 2020. Last year's slump was of comparable magnitude, except for China, so we should still be about 10% below 2019 levels. EU tariffs protect against Asian competition; prices in China have risen more moderately than in Europe since the beginning of the year.

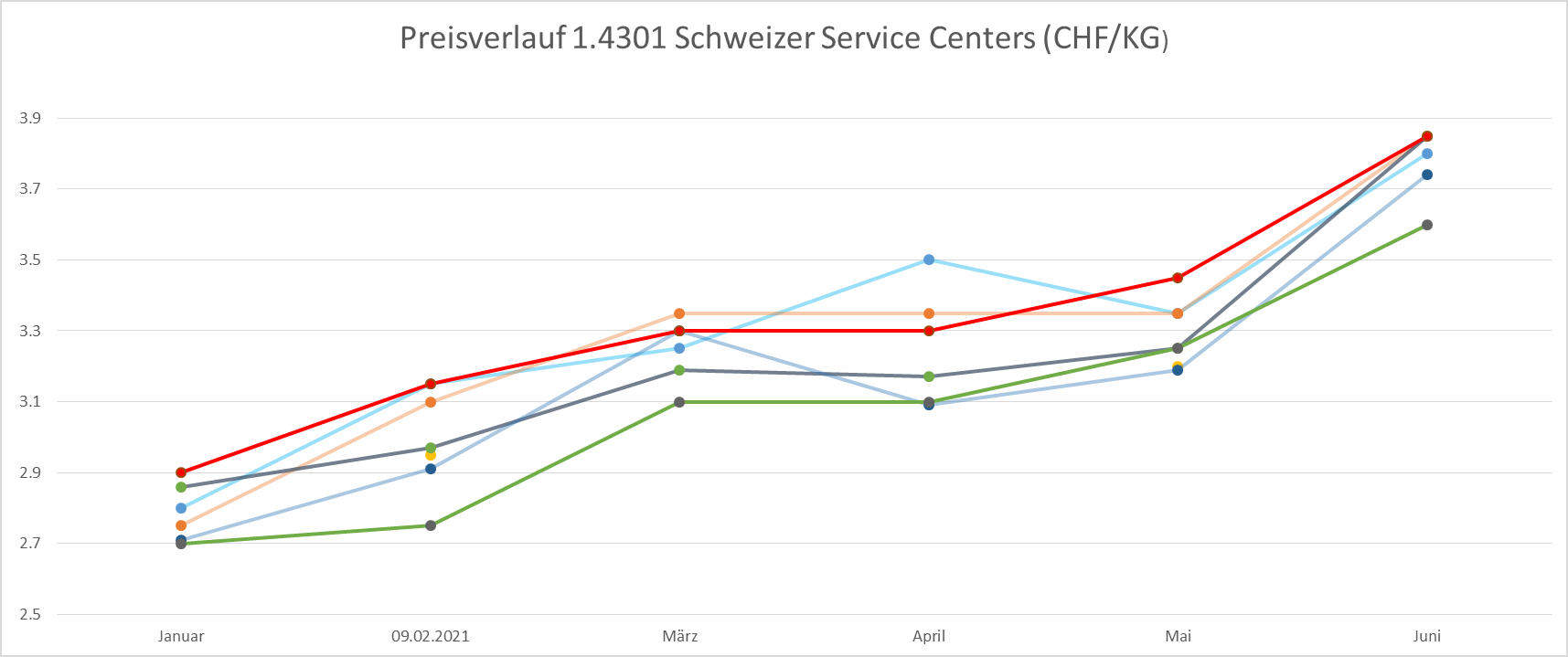

Price development 304L Swiss Service Centers

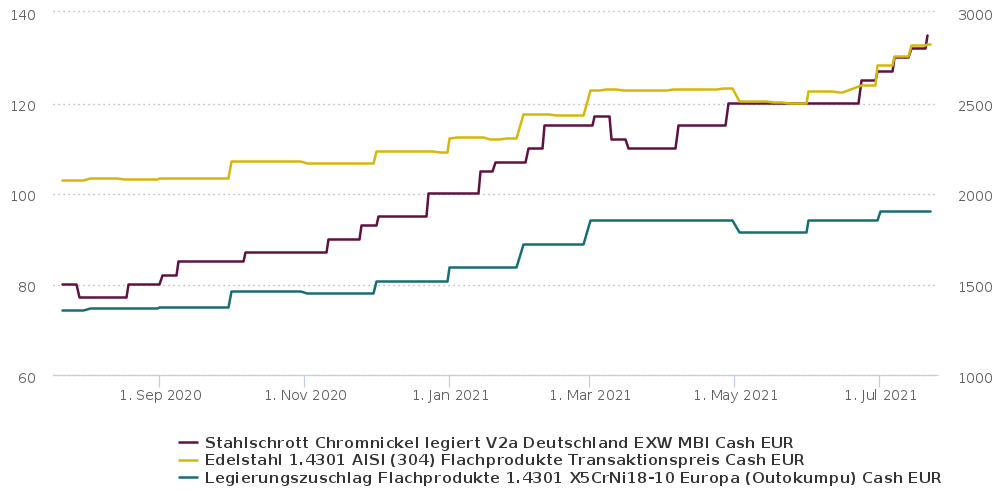

Stocks are at a very low level in Europe and factory delivery times are well over 6 months. The factories can utilise capacity well, but are certainly not yet at full capacity. Other capacity-limiting factors, such as financing, logistical problems and, more recently, freak weather, also play a role. The general shortage of materials is helped by the fact that certain industries, such as aviation or the chemical process industry, have not yet reached pre-crisis levels by a long shot. Nevertheless, the situation should calm down after the summer. In particular, the mills' base prices will return to a normal level. Alloy surcharges, on the other hand, could increase further, especially in the higher-alloy materials. However, there is also a lot going on the sidelines, packaging costs and above all freight rates are rising continuously: "According to Drewry, a container on the important export route from Shanghai to Rotterdam now already costs around 12,000 dollars. The figure seems almost absurd. Just a year ago, a container transport from Asia to Northern Europe would not even have cost $2,000." (WiWo 21 June 2021)It is also worth taking a look at the scrap price development (left scale in the chart) compared to the stainless steel prices (right scale). This shows once again that scrap is the most important raw material for our industry and its scarcity has a price-driving influence. More on this topic is also on the Hempel page.

Stainless steel 304L € prices

There is a stronger increase in scrap prices (+ 60%) compared to transaction prices (+ 40%).

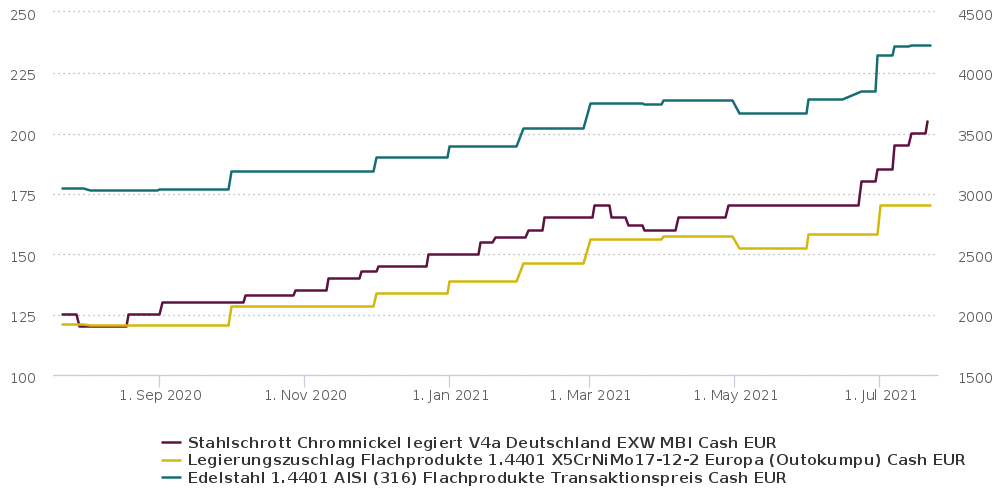

Stainless steel 316L € prices

We expect a more moderate price development after the summer; except in titanium, where the rally will only begin. If the forecasts are correct that the consumption of nickel for the use in batteries will increase by 500% in the next few years (CCO from BHP), we will also be facing more difficult times in the medium term for nickel alloys. Hempel's nitrogen-alloyed stainless steels might help.

Chart-Source: MBI Metal Source